Will Higher Gmv & Consumers Help Affirm Boost Q3 Earnings?

Leading buy now, pay later (BNPL) solution provider Affirm Holdings, Inc. AFRM is set to report its third-quarter fiscal 2026 results on May 7, 2026, after the closing bell. The Zacks Consensus Estimate for the to-be-reported quarter’s bottom line is currently pegged at an earnings of 17 cents per share on revenues of $997.92 million.

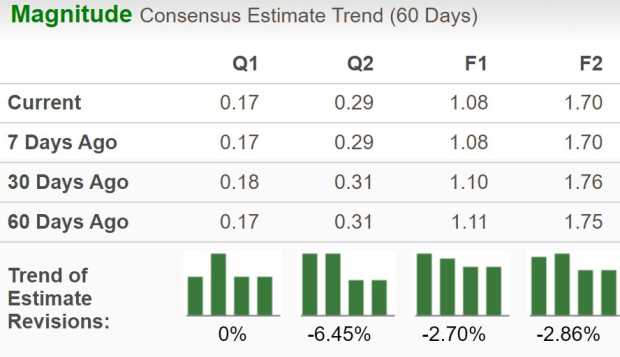

The fiscal third-quarter earnings estimate has remained stable over the past 60 days. The bottom-line projection indicates a massive year-over-year jump from a penny. Also, the Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of 27.4%.

Image Source: Zacks Investment Research

For fiscal 2026, the Zacks Consensus Estimate for Affirm’s revenues is pegged at $4.14 billion, implying a rise of 28.5% year over year. The consensus mark for the current fiscal year’s EPS is pegged at $1.08, implying a massive improvement from 15 cents a year ago.

Affirm beat the consensus estimate for earnings in each of the last four quarters, with the average surprise being 83.5%.

Affirm Holdings, Inc. Price and EPS Surprise

Affirm Holdings, Inc. price-eps-surprise | Affirm Holdings, Inc. Quote

Affirm’s Q3 Earnings Whispers

However, our proven model does not conclusively predict an earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That’s not the case here.

AFRM currently has an Earnings ESP of -16.24% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Now, let’s see how things have shaped up before the fiscal third-quarter earnings announcement.

Q3 Factors to Note for Affirm

Merchant network revenues are likely to have benefited from an expanding Gross Merchandise Volume (GMV). The active merchants figure is expected to have witnessed a significant boost in the fiscal third quarter due to the company’s ability to strike deals with different businesses. The Zacks Consensus Estimate for merchant network revenues is pegged at $271.7 million, indicating a 27% rise from the prior-year quarter’s figure.

The consensus mark for GMV for the fiscal third quarter implies 30.3% growth from the prior-year quarter’s number. Management anticipates the metric to be in the range of $11-$11.25 billion.

An increase in the number of transactions conducted through the Affirm platform is likely to have been supported by higher active merchants and consumers. The Zacks Consensus Estimate for active consumers indicates 20.7% year-over-year growth. The consensus mark for transactions per active consumer suggests a 12.9% rise from the year-ago period.

An increase in the usage of Affirm’s virtual cards is expected to have driven card network revenues. The consensus mark for card network revenues indicates a 24.4% improvement from the year-ago quarter’s number. Meanwhile, the Zacks Consensus Estimate for interest income is pegged at $504.1 million, which implies a 25.2% year-over-year rise.

The consensus mark for servicing income is pegged at $44.6 million, which indicates a 39.3% jump from the year-ago quarter. However, the quarterly results are likely to have witnessed higher transaction costs. Yet, the company expects the adjusted operating margin to be within 24.5-25.5%.

How Did Other Payments Companies Perform?

Companies like Visa Inc. V, Mastercard Incorporated MA and American Express Company AXP have already announced results for the March quarter. Here’s how they have performed:

Visa delivered second-quarter fiscal 2026 adjusted earnings of $3.31 per share, up 20% year over year and ahead of the Zacks Consensus Estimate by 7.1%. Its strong quarterly results reflected resilient spending trends, higher cross-border volumes andsolid network activity, including an increase in payments volume.However, the upside was partly offset by Visa’s increased operating expenses.

Mastercard reported first-quarter 2026 adjusted earnings of $4.60 per share, which topped the Zacks Consensus Estimate by 4.6% and increased 23.3% year over year. Its results benefited from growing cross-border volumes and solid growth in value-added services revenues. However, the upside was partly offset by Mastercard’s elevated operating expenses and higher payment network rebates from new and renewed deals.

American Express reported first-quarter 2026 EPS of $4.28, which surpassed the Zacks Consensus Estimate by 6.2% and advanced 18% year over year. Its quarterly results were driven by increased Card Member spending, higher net interest income and improved card fee growth. However, the upside was partly offset by AXP’s elevated operating expenses.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).

Popular Products

-

Classic Oversized Teddy Bear

Classic Oversized Teddy Bear$23.78 -

Gem's Ballet Natural Garnet Gemstone ...

Gem's Ballet Natural Garnet Gemstone ...$171.56$85.78 -

Butt Lifting Body Shaper Shorts

Butt Lifting Body Shaper Shorts$95.56$47.78 -

Slimming Waist Trainer & Thigh Trimmer

Slimming Waist Trainer & Thigh Trimmer$67.56$33.78 -

Realistic Fake Poop Prank Toys

Realistic Fake Poop Prank Toys$99.56$49.78