Smucker Trends Show Sjm Chasing Growth Beyond The Grocery Aisle

The J. M. Smucker Company SJM is trying to make its next phase less dependent on mature grocery categories. The company is leaning into foodservice channels, convenience-led formats, premium coffee and productivity-led margin recovery.

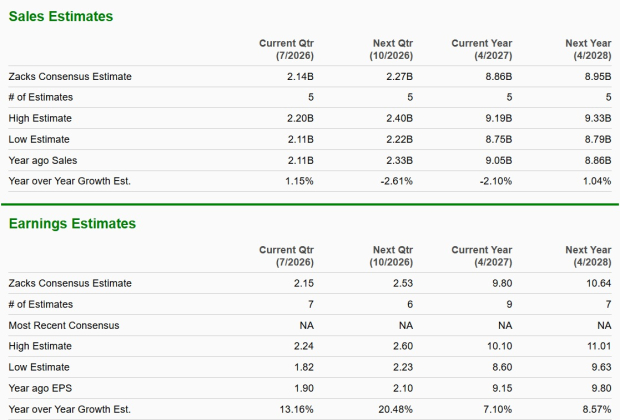

Fiscal 2027 sales are expected to decline 3% to 4%, so investors need proof priority platforms can offset softer demand elsewhere.

How SJM Is Expanding Beyond Retail Shelves

Away From Home is the clearest sign that Smucker is pushing beyond traditional retail shelves. The business serves schools, workplaces, lodging, healthcare, convenience stores and restaurants, giving SJM more ways to reach consumers.

The segment became separately reportable in fiscal 2026, signaling that it is now large enough to influence the company narrative. Fourth-quarter Away From Home sales rose 15%, driven by coffee, Uncrustables, fruit spreads and foodservice demand.

The Kraft Heinz Company KHC is relevant because packaged food companies are also looking for growth beyond center-store exposure. Smucker’s channel mix gives investors another test of how legacy brands can find new occasions.

Why Smucker Is Betting on Convenience

Uncrustables is the lead example of Smucker’s convenience strategy. The brand reached $1 billion in annual sales, added about 3 million households over the past year and still has household penetration of only 27%.

The product strategy is built around more eating moments. Fridge-friendly Uncrustables can stay fresh in the refrigerator for up to five days, while breakfast varieties with 12 grams of protein extend the brand into morning usage.

Image Source: Zacks Investment Research

How Coffee Trends Favor SJM Margins

Cafe Bustelo gives Smucker a faster-growing coffee platform inside a mature category. The brand grew net sales 39% in fiscal 2026 within U.S. Retail Coffee and reached about $550 million in sales.

Growth is supported by expansion in the Central and West Coast regions, differentiated roast profiles, innovation and marketing aimed at a broader audience while preserving its Latin roots. Management has also cited resonance with Gen Z and Millennial consumers.

Coffee also shapes the margin story. Green coffee deflation is expected to weigh on sales as lower costs are passed through, but it is expected to help profitability, with productivity actions supporting adjusted gross margin of about 38% in fiscal 2027. Tariffs remain a watchpoint because guidance does not assume impacts from new or changed tariffs.

Where Smucker Still Faces Demand Friction

Not every category is participating equally. Sweet Baked Snacks remains a stabilization project after fiscal 2026 segment sales fell 18% and segment profit declined nearly 56%.

Pet foods also remain uneven. Cat food has momentum, but dog snacks and the lapping of contract manufacturing sales tied to divested pet food brands weighed on fiscal 2026 U.S. Retail Pet Foods sales.

General Mills, Inc. GIS is a useful comparison because it also has exposure to packaged foods and pet. For SJM, the key issue is whether pet can move from selective improvement to broader volume support.

What SJM Spending Says About Priorities

Smucker is putting more money behind the brands it wants to lead the next phase. Selling, distribution and administrative expenses are projected to rise about 5% in fiscal 2027, with marketing expense expected at 5.7% of sales.

That spending is focused on Uncrustables, Cafe Bustelo, Meow Mix and Milk-Bone. The logic is clear, but the payoff still has to show up in durable volume growth during a year when lower pricing and softer volume/mix are expected to pressure sales.

The J. M. Smucker Company Price, Consensus and EPS Surprise

The J. M. Smucker Company price-consensus-eps-surprise-chart | The J. M. Smucker Company Quote

How Smucker Signals Frame the Trend Trade

The bottom line is that SJM has credible trend support, but the stock still reads as a neutral trend trade. Channel diversification, convenience innovation, premium coffee and margin recovery all help, but fiscal 2027 sales visibility remains weak.

The stock currently carries a Zacks Rank #3 (Hold). It also has a Value Score of B, Growth Score of A, Momentum Score of A and VGM Score of A, giving investors favorable style signals to compare with the hold-ranked earnings-revision backdrop. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores are designed to complement the Zacks Rank, not replace it. For SJM, that means favorable grades support monitoring the trend case, while the Zacks Rank #3 keeps the near-term stance measured until sales and execution improve.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).

Popular Products

-

Classic Oversized Teddy Bear

Classic Oversized Teddy Bear$23.78 -

Gem's Ballet Natural Garnet Gemstone ...

Gem's Ballet Natural Garnet Gemstone ...$171.56$85.78 -

Butt Lifting Body Shaper Shorts

Butt Lifting Body Shaper Shorts$95.56$47.78 -

Slimming Waist Trainer & Thigh Trimmer

Slimming Waist Trainer & Thigh Trimmer$67.56$33.78 -

Realistic Fake Poop Prank Toys

Realistic Fake Poop Prank Toys$99.56$49.78